0001487198falseFY2022P6Y00014871982021-05-012022-04-3000014871982021-10-29iso4217:USD00014871982022-07-22xbrli:shares00014871982022-04-3000014871982021-04-300001487198aspu:ComputerEquipmentAndHardwareMember2022-04-300001487198aspu:ComputerEquipmentAndHardwareMember2021-04-300001487198us-gaap:FurnitureAndFixturesMember2022-04-300001487198us-gaap:FurnitureAndFixturesMember2021-04-300001487198us-gaap:LeaseholdImprovementsMember2022-04-300001487198us-gaap:LeaseholdImprovementsMember2021-04-300001487198aspu:InstructionalEquipmentMember2022-04-300001487198aspu:InstructionalEquipmentMember2021-04-300001487198us-gaap:ComputerSoftwareIntangibleAssetMember2022-04-300001487198us-gaap:ComputerSoftwareIntangibleAssetMember2021-04-300001487198us-gaap:ConstructionInProgressMember2022-04-300001487198us-gaap:ConstructionInProgressMember2021-04-300001487198aspu:IntangibleAssetsOtherThanCoursewareAndAccreditationMember2022-04-300001487198aspu:IntangibleAssetsOtherThanCoursewareAndAccreditationMember2021-04-300001487198aspu:CoursewareAndAccreditationMember2022-04-300001487198aspu:CoursewareAndAccreditationMember2021-04-30iso4217:USDxbrli:shares00014871982020-05-012021-04-300001487198us-gaap:CommonStockMember2020-04-300001487198us-gaap:AdditionalPaidInCapitalMember2020-04-300001487198us-gaap:TreasuryStockMember2020-04-300001487198us-gaap:RetainedEarningsMember2020-04-3000014871982020-04-300001487198us-gaap:AdditionalPaidInCapitalMember2020-05-012021-04-300001487198us-gaap:CommonStockMember2020-05-012021-04-300001487198us-gaap:TreasuryStockMember2020-05-012021-04-300001487198us-gaap:RetainedEarningsMember2020-05-012021-04-300001487198us-gaap:CommonStockMember2021-04-300001487198us-gaap:AdditionalPaidInCapitalMember2021-04-300001487198us-gaap:TreasuryStockMember2021-04-300001487198us-gaap:RetainedEarningsMember2021-04-300001487198us-gaap:AdditionalPaidInCapitalMember2021-05-012022-04-300001487198us-gaap:CommonStockMember2021-05-012022-04-300001487198srt:DirectorMemberus-gaap:CommonStockMember2021-05-012022-04-300001487198us-gaap:RetainedEarningsMember2021-05-012022-04-300001487198us-gaap:CommonStockMember2022-04-300001487198us-gaap:AdditionalPaidInCapitalMember2022-04-300001487198us-gaap:TreasuryStockMember2022-04-300001487198us-gaap:RetainedEarningsMember2022-04-30aspu:subsidiary0001487198aspu:CollateralPledgedStateOfArizonaMember2022-04-300001487198us-gaap:SuretyBondMemberaspu:CollateralPledgedStateOfArizonaMember2022-04-300001487198aspu:CollateralPledgedAspenUniversityLetterOfCreditMember2022-04-300001487198aspu:CollateralPledgedBankLetterOfCreditMember2022-04-300001487198aspu:SecuredCreditLineMember2022-04-300001487198aspu:CollateralPledgedAspenUniversityLetterOfCreditMember2021-04-300001487198aspu:CollateralPledgedBankLetterOfCreditMember2021-04-30aspu:reporting_unitxbrli:pure0001487198aspu:ComputerEquipmentAndHardwareMember2021-05-012022-04-300001487198us-gaap:ComputerSoftwareIntangibleAssetMember2021-05-012022-04-300001487198aspu:InstructionalEquipmentMember2021-05-012022-04-300001487198us-gaap:FurnitureAndFixturesMember2021-05-012022-04-300001487198srt:MaximumMemberus-gaap:LeaseholdImprovementsMember2021-05-012022-04-300001487198aspu:CoursewareAndAccreditationMember2021-05-012022-04-300001487198us-gaap:CommonStockMemberaspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2021-05-012022-04-300001487198aspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2020-04-300001487198us-gaap:CommonStockMemberaspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2020-08-012020-10-31aspu:segment0001487198aspu:UnbilledEducationalServicesMember2021-04-300001487198us-gaap:ComputerSoftwareIntangibleAssetMember2022-04-300001487198us-gaap:ComputerSoftwareIntangibleAssetMember2021-04-300001487198aspu:CoursewareMember2022-04-300001487198aspu:CoursewareMember2021-04-300001487198aspu:AccreditationMember2022-04-300001487198aspu:AccreditationMember2021-04-300001487198aspu:CoursewareAndAccreditationMember2020-05-012021-04-300001487198aspu:HemgMember2021-05-012022-04-300001487198us-gaap:RevolvingCreditFacilityMemberaspu:CreditFacilityDueMarchFourteenTwoThousandTwentyThreeMemberus-gaap:LineOfCreditMember2022-04-300001487198us-gaap:RevolvingCreditFacilityMemberaspu:CreditFacilityDueMarchFourteenTwoThousandTwentyThreeMemberus-gaap:LineOfCreditMember2021-04-300001487198aspu:CreditFacilityDueNovemberFourTwoThousandTwentyThreeMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-04-300001487198aspu:CreditFacilityDueNovemberFourTwoThousandTwentyThreeMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2021-04-300001487198us-gaap:ConvertibleNotesPayableMemberaspu:TwentyTwentyTwoConvertibleNotesMember2022-03-140001487198us-gaap:ConvertibleNotesPayableMemberaspu:TwentyTwentyTwoConvertibleNotesMember2022-04-300001487198us-gaap:ConvertibleNotesPayableMemberaspu:TwentyTwentyTwoConvertibleNotesMember2021-04-300001487198aspu:TwentyTwentyTwoConvertibleNotesMember2022-03-1400014871982022-03-14aspu:unaffiliated_lender0001487198us-gaap:ConvertibleDebtMemberaspu:TwentyTwentyTwoConvertibleNotesMember2022-03-140001487198us-gaap:ConvertibleNotesPayableMemberaspu:TwentyTwentyTwoConvertibleNotesMember2022-03-142022-03-14utr:D0001487198aspu:TwentyTwentyTwoConvertibleNotesMember2022-03-142022-03-140001487198us-gaap:RevolvingCreditFacilityMemberaspu:TwoThousandTwentyTwoRevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-03-142022-03-140001487198us-gaap:RevolvingCreditFacilityMemberaspu:TwoThousandTwentyTwoRevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-03-140001487198us-gaap:RevolvingCreditFacilityMemberaspu:TwoThousandTwentyTwoRevolvingCreditFacilityMember2021-04-300001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMember2022-03-142022-03-1400014871982022-04-220001487198aspu:IntercreditorAgreementMember2022-04-22aspu:lender0001487198us-gaap:RevolvingCreditFacilityMember2022-04-220001487198us-gaap:WarrantMemberaspu:IntercreditorAgreementMember2022-04-220001487198us-gaap:WarrantMemberaspu:IntercreditorAgreementMember2022-04-222022-04-220001487198us-gaap:RevolvingCreditFacilityMemberaspu:TwoThousandTwentyTwoRevolvingCreditFacilityMember2022-04-300001487198aspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2020-01-22aspu:note0001487198aspu:ConvertibleNotesMemberus-gaap:RevolvingCreditFacilityMember2018-11-050001487198aspu:ConvertibleNotesMemberus-gaap:RevolvingCreditFacilityMember2020-01-222020-01-220001487198aspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2020-09-140001487198aspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2020-09-142020-09-140001487198us-gaap:ConvertibleDebtMember2020-09-142020-09-140001487198aspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2020-08-012020-10-310001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMember2018-11-050001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMembersrt:MinimumMember2018-11-050001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMember2021-08-312021-08-310001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMember2022-04-300001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMember2021-04-300001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:WarrantMember2021-08-310001487198us-gaap:WarrantMember2021-08-310001487198aspu:TwoThousandEighteenCreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMembersrt:MaximumMember2022-03-1400014871982013-02-110001487198aspu:HemgMember2015-09-290001487198aspu:HemgMember2021-07-212021-07-210001487198aspu:HemgMember2021-05-012021-07-3100014871982021-04-162021-04-1600014871982020-01-012020-12-3100014871982021-01-012021-12-310001487198aspu:PhoenixArizonaMember2022-02-28aspu:employee00014871982022-03-012022-03-310001487198us-gaap:SubsequentEventMember2022-06-30aspu:phaseaspu:quarteraspu:state0001487198us-gaap:CustomerConcentrationRiskMemberaspu:TitleIVProgramsAspenUniversityMemberus-gaap:SalesRevenueNetMember2020-05-012021-04-300001487198us-gaap:CustomerConcentrationRiskMemberaspu:TitleIVProgramsUnitedStatesUniversityMemberus-gaap:SalesRevenueNetMember2020-05-012021-04-300001487198aspu:UsuMemberus-gaap:LetterOfCreditMember2016-12-310001487198aspu:CollateralPledgedBankLetterOfCreditMember2020-09-280001487198aspu:CollateralPledgedBankLetterOfCreditMember2020-08-310001487198aspu:CollateralPledgedBankLetterOfCreditMember2020-12-31aspu:plan00014871982022-03-082022-03-080001487198aspu:A2018EquityIncentivePlanMember2022-04-300001487198aspu:A2012And2018EquityIncentivePlanMember2021-04-300001487198aspu:A2018EquityIncentivePlanMember2020-12-300001487198aspu:A2018EquityIncentivePlanMember2021-12-220001487198us-gaap:SubsequentEventMember2022-07-050001487198us-gaap:SubsequentEventMember2022-07-060001487198us-gaap:PreferredStockMembersrt:MaximumMember2022-04-300001487198aspu:EquityDistributionAgreementMember2020-08-310001487198aspu:EquityDistributionAgreementMember2020-05-012021-04-300001487198aspu:EquityDistributionAgreementMember2020-08-312020-08-310001487198srt:DirectorMemberus-gaap:CommonStockMember2022-01-032022-01-030001487198srt:DirectorMemberus-gaap:CommonStockMember2022-01-030001487198us-gaap:CommonStockMemberaspu:FormerDirectorMember2020-05-012021-04-30aspu:day0001487198us-gaap:CommonStockMemberaspu:ConvertibleNotesMemberus-gaap:ConvertibleNotesPayableMember2020-09-142020-09-140001487198us-gaap:RestrictedStockMember2022-04-300001487198us-gaap:RestrictedStockMember2021-04-300001487198us-gaap:RestrictedStockUnitsRSUMember2021-04-300001487198us-gaap:RestrictedStockUnitsRSUMember2021-05-012022-04-300001487198us-gaap:RestrictedStockUnitsRSUMember2022-04-300001487198us-gaap:ShareBasedPaymentArrangementEmployeeMemberus-gaap:RestrictedStockUnitsRSUMember2021-05-012022-04-300001487198srt:ChiefFinancialOfficerMemberus-gaap:RestrictedStockUnitsRSUMember2021-08-162021-08-160001487198srt:ChiefFinancialOfficerMemberus-gaap:RestrictedStockUnitsRSUMember2021-08-160001487198aspu:ChiefAcademicOfficerMemberus-gaap:RestrictedStockUnitsRSUMember2021-08-122021-08-120001487198srt:ChiefOperatingOfficerMemberus-gaap:RestrictedStockUnitsRSUMember2021-08-122021-08-120001487198us-gaap:RestrictedStockUnitsRSUMember2021-08-120001487198aspu:A2018EquityIncentivePlanMemberus-gaap:RestrictedStockUnitsRSUMember2021-05-012022-04-300001487198us-gaap:RestrictedStockUnitsRSUMembersrt:ChiefExecutiveOfficerMember2021-07-212021-07-210001487198us-gaap:RestrictedStockUnitsRSUMembersrt:ChiefExecutiveOfficerMember2021-07-210001487198us-gaap:RestrictedStockUnitsRSUMembersrt:ChiefExecutiveOfficerMember2021-05-012022-04-300001487198aspu:EmployeesMemberus-gaap:RestrictedStockUnitsRSUMember2021-05-012022-04-300001487198aspu:EmployeesMemberus-gaap:RestrictedStockUnitsRSUMembersrt:MinimumMember2021-05-012022-04-300001487198aspu:EmployeesMemberus-gaap:RestrictedStockUnitsRSUMembersrt:MaximumMember2021-05-012022-04-300001487198aspu:EmployeesMemberus-gaap:RestrictedStockUnitsRSUMember2022-04-300001487198us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2020-02-040001487198us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2020-02-042020-02-0400014871982020-02-040001487198us-gaap:RestrictedStockUnitsRSUMember2020-05-012021-04-300001487198aspu:BoardOfDirectorsMemberus-gaap:RestrictedStockUnitsRSUMember2020-11-012021-01-310001487198us-gaap:RestrictedStockUnitsRSUMembersrt:MinimumMember2020-05-012021-04-300001487198us-gaap:RestrictedStockUnitsRSUMembersrt:MaximumMember2020-05-012021-04-300001487198us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2021-04-300001487198us-gaap:WarrantMember2021-04-300001487198us-gaap:WarrantMember2021-04-302021-04-300001487198us-gaap:WarrantMember2021-05-012022-04-300001487198us-gaap:WarrantMember2022-04-300001487198us-gaap:WarrantMember2022-04-302022-04-300001487198us-gaap:WarrantMemberaspu:A100Member2021-05-012022-04-300001487198us-gaap:WarrantMemberaspu:A100Member2022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeNineMemberus-gaap:WarrantMember2021-05-012022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeNineMemberus-gaap:WarrantMember2022-04-300001487198us-gaap:WarrantMemberaspu:A585Member2021-05-012022-04-300001487198us-gaap:WarrantMemberaspu:A585Member2022-04-300001487198aspu:A600Memberus-gaap:WarrantMember2021-05-012022-04-300001487198aspu:A600Memberus-gaap:WarrantMember2022-04-300001487198us-gaap:WarrantMemberaspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeElevenMember2021-05-012022-04-300001487198us-gaap:WarrantMemberaspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeElevenMember2022-04-300001487198us-gaap:WarrantMemberaspu:A699Member2021-05-012022-04-300001487198us-gaap:WarrantMemberaspu:A699Member2022-04-300001487198us-gaap:WarrantMemberus-gaap:WarrantMember2022-04-300001487198us-gaap:RevolvingCreditFacilityMemberus-gaap:WarrantMemberaspu:TwoThousandTwentyTwoRevolvingCreditFacilityMember2022-04-250001487198us-gaap:WarrantMember2022-04-250001487198us-gaap:WarrantMemberaspu:LeonAndTobyCoopermanFamilyFoundationMember2021-08-310001487198us-gaap:WarrantMemberaspu:LeonAndTobyCoopermanFamilyFoundationMember2021-08-312021-08-310001487198aspu:CreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:WarrantMember2021-08-310001487198us-gaap:WarrantMemberaspu:LeonAndTobyCoopermanFamilyFoundationMember2021-05-012022-04-300001487198us-gaap:WarrantMemberaspu:FormerBoardOfDirectorMember2021-07-210001487198us-gaap:WarrantMemberaspu:FormerBoardOfDirectorMember2021-07-212021-07-210001487198us-gaap:WarrantMemberaspu:FormerBoardOfDirectorMember2021-05-012022-04-300001487198aspu:CoopermanWarrantsMember2020-06-052020-06-050001487198aspu:CreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMemberaspu:CoopermanWarrantsMember2018-11-050001487198aspu:CreditFacilityAgreementMemberus-gaap:RevolvingCreditFacilityMemberaspu:CoopermanWarrantsMember2020-06-050001487198aspu:CoopermanWarrantsMemberaspu:LoanAgreementsMember2019-03-062019-03-060001487198aspu:CoopermanWarrantsMemberaspu:LoanAgreementsMember2020-06-052020-06-050001487198aspu:CoopermanWarrantsMember2020-06-0800014871982020-05-012020-07-310001487198aspu:StockOptionGrantsToEmployeesAndDirectorsMember2021-05-012022-04-300001487198aspu:StockOptionGrantsToEmployeesAndDirectorsMember2020-05-012021-04-300001487198aspu:StockOptionGrantsToEmployeesAndDirectorsMember2021-04-300001487198aspu:StockOptionGrantsToEmployeesAndDirectorsMember2021-04-302021-04-300001487198aspu:StockOptionGrantsToEmployeesAndDirectorsMember2022-04-300001487198aspu:StockOptionGrantsToEmployeesAndDirectorsMember2022-04-302022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeThreeMember2021-05-012022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeThreeMember2022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeFourMember2021-05-012022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeFourMember2022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeFiveMember2021-05-012022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeFiveMember2022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeSixMember2021-05-012022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeSixMember2022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeSevenMember2021-05-012022-04-300001487198aspu:ShareBasedCompensationSharesAuthorizedUnderStockOptionPlansExercisePriceRangeSevenMember2022-04-300001487198us-gaap:EmployeeStockOptionMember2021-05-012022-04-300001487198us-gaap:RestrictedStockMember2021-05-012022-04-300001487198us-gaap:RestrictedStockMember2020-05-012021-04-300001487198us-gaap:EmployeeStockOptionMember2020-05-012021-04-3000014871982020-10-162020-10-160001487198us-gaap:TreasuryStockMember2020-10-162020-10-16utr:sqft0001487198srt:MinimumMember2022-04-300001487198srt:MaximumMember2022-04-300001487198aspu:TampaFloridaMember2022-04-300001487198aspu:TuitionRevenueMember2021-05-012022-04-300001487198aspu:TuitionRevenueMember2020-05-012021-04-300001487198aspu:CourseFeeRevenueMember2021-05-012022-04-300001487198aspu:CourseFeeRevenueMember2020-05-012021-04-300001487198aspu:BookFeeRevenueMember2021-05-012022-04-300001487198aspu:BookFeeRevenueMember2020-05-012021-04-300001487198aspu:ExamFeeRevenueMember2021-05-012022-04-300001487198aspu:ExamFeeRevenueMember2020-05-012021-04-300001487198aspu:ServiceFeeRevenueMember2021-05-012022-04-300001487198aspu:ServiceFeeRevenueMember2020-05-012021-04-300001487198us-gaap:CustomerConcentrationRiskMemberus-gaap:NonUsMemberus-gaap:SalesRevenueNetMember2021-05-012022-04-300001487198us-gaap:CustomerConcentrationRiskMemberus-gaap:NonUsMemberus-gaap:SalesRevenueNetMember2020-05-012021-04-300001487198aspu:TaxYear2013To2021Member2022-04-300001487198us-gaap:TaxYear2022Member2022-04-3000014871982021-05-012021-07-3100014871982021-08-012021-10-3100014871982021-11-012022-01-3100014871982022-02-012022-04-3000014871982020-08-012020-10-3100014871982020-11-012021-01-3100014871982021-02-012021-04-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K | | | | | |

☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended April 30, 2022 |

or | | | | | |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ___________ to ___________ |

Commission file number 001-38175

ASPEN GROUP, INC.

(Exact Name of Registrant as Specified in Its Charter) | | | | | | | | |

| Delaware | | 27-1933597 |

| State or Other Jurisdiction of Incorporation or Organization | | I.R.S. Employer Identification No. |

| | |

276 Fifth Avenue, Suite 505, New York, New York | | 10001 |

| Address of Principal Executive Offices | | Zip Code |

(646) 448-5144

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, par value $0.001 | ASPU | The Nasdaq Stock Market (The Nasdaq Global Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. | | | | | | | | | | | |

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer ☑ | Smaller reporting company ☑ | |

| Emerging growth company ☐ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. Approximately $112 million based on a closing price of $4.75 on October 29, 2021.

The number of shares outstanding of the registrant’s classes of common stock, as of July 22, 2022 was 25,202,278 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's proxy statement for the 2022 Annual Meeting of Shareholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K to the extent stated herein.

PART I

ITEM 1. BUSINESS.

Aspen Group, Inc. is an education technology holding company. AGI has two subsidiaries, Aspen University Inc. ("Aspen University" or "AU") organized in 1987 and United States University Inc. ("United States University" or "USU").

All references to the “Company”, “AGI”, “Aspen Group”, “we”, “our” and “us” refer to Aspen Group, Inc., unless the context otherwise indicates.

Description of Business

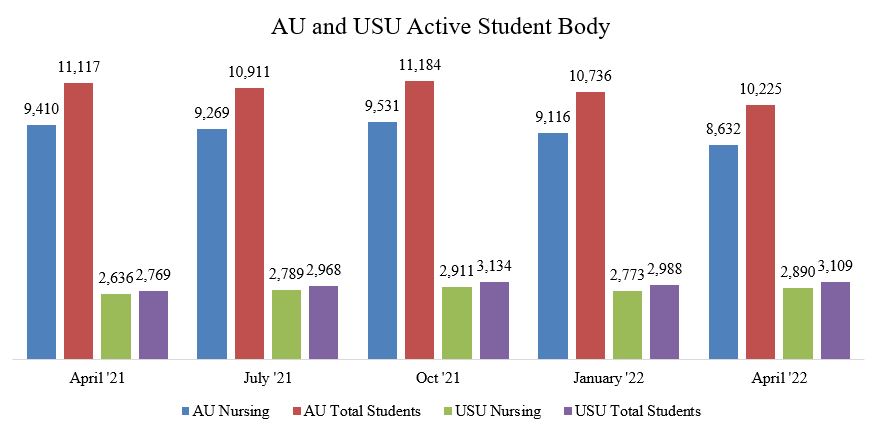

AGI leverages its education technology infrastructure and expertise to allow its two universities, Aspen University and United States University, to deliver on the vision of making college affordable again. Because we believe higher education should be a catalyst to our students’ long-term economic success, we exert financial prudence by offering affordable tuition that is one of the greatest values in higher education. AGI’s primary focus relative to future growth is to target the high growth nursing profession. As of April 30, 2022, 11,522 of 13,334 or 86% of all active students across both universities are degree-seeking nursing students. Of the students seeking nursing degrees, 9,562 are RNs studying to earn an advanced degree, including 6,672 at Aspen University and 2,890 at USU. In contrast, the remaining 1,960 nursing students are enrolled in Aspen University’s BSN Pre-Licensure program in the Phoenix, Austin, Tampa, Nashville and Atlanta metros.

Aspen University has been offering a monthly payment plan available to all students across every online degree program offered by Aspen University, since March 2014. The monthly payment plan is designed so that students will make one fixed payment per month, and that monthly payment is applied towards the total cost of attendance (tuition and fees, excluding textbooks). The monthly payment plan offers online undergraduate students the opportunity to pay their tuition and fees at $250/month, online master students $325/month, and online doctoral students $375/month, interest free, thereby giving students a monthly payment option versus taking out a federal financial aid loan.

USU has been offering monthly payment plans since the summer of 2017. Today, USU monthly payment plans are available for the online RN to BSN program ($250/month), online MBA/MAEd/MSN programs ($325/month), online hybrid Bachelor of Arts in Liberal Studies, Teacher Credentialing tracks approved by the California Commission on Teacher Credentialing ($350/month), and the online hybrid Master of Science in Nursing-Family Nurse Practitioner (“FNP”) program ($375/month).

Fiscal 2022 Overview

For Fiscal Year 2022, the Company achieved and experienced the following key developments:

Aspen 2.0 Business Plan and Other Trends

In Fiscal Year 2022, the Company implemented its ‘Aspen 2.0’ business plan. Aspen 2.0 is designed to deliver maximum efficiency as defined by revenue earned from each marketing dollar spent. Under the plan, growth spending has been re-focused on our highest efficiency businesses in an effort to accelerate the growth in these units, with decreased spending in our lowest efficiency unit (an area where high growth is not essential). Specifically, we have reduced marketing spending in our traditional AU Nursing + Other unit. In addition, we have suspended spending in our Phoenix metro BSN Pre-Licensure, as it was nearing capacity and also more recently due to regulatory issues described beginning at page 1 of this Report. Those marketing dollars have been redirected towards high LTV programs, specifically our four new BSN Pre-Licensure metros, AU’s online doctoral programs, and USU's MSN-FNP program. Additionally, due to a requirement to collateralize a new surety bond required by the Arizona State Board for Private Postsecondary Education, the Company reduced marketing spend in the fourth quarter of fiscal year 2022 compared to immediately preceding periods. While this resulted in improved operating results for that quarter, we may see negative trends in future periods if the decrease in marketing spend results in a decline in enrollments. In the Phoenix metro, which was profitable, we cannot currently matriculate pre-professional nursing students into the two-year core nursing program. See Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Arizona State Board of Nursing Probation

Because Aspen University’s first-time pass rates for our BSN pre-licensure students taking the NCLEX-RN exam in Arizona fell from 80% in 2020 to 58% in 2021, which is below the minimum 80% standard set by the Arizona State Board of Nursing (“AZ BON”) in March 2022, AU entered into a Consent Agreement for Probation and a Civil Penalty (the “Consent Agreement”) with the AZ BON pursuant to which AU’s Provisional Approval was revoked, with the revocation stayed pending

AU’s compliance with the terms and conditions of the Consent Agreement. The minimum probationary period is 36 months from the date of the Consent Agreement. In June 2022, the AZ BON granted approval of Aspen University’s request for provisional approval as long as the program is in compliance with the consent agreement through March 31, 2025. Aspen University is not currently enrolling students in the BSN Pre-licensure program in Arizona.

Because the pre-licensure program is comprised of two components, a one-year pre-requisite Pre-Professional Nursing (“PPN”) requirement followed by a two-year core program, one effect of the foregoing events was to prevent PPN students from matriculating into the core program until after the probation stipulation is met.

See “State Professional Licensure” on page 10 for more information on the Consent Agreement and Civil Penalty, and “Item 3 - Legal Proceedings” for more information on a class action lawsuit filed after disclosure of the Consent Agreement.

Stipulated Agreement and Surety Bond

In connection with the above developments with respect to the AZ BON, Aspen University has also entered into a Stipulated Agreement with the Arizona State Board for Private Postsecondary Education (the “Arizona Board”) which required us to post a surety bond for $18.3 million. Aspen University posted the surety bond on April 22, 2022. Aspen University is not currently enrolling students in the BSN Pre-licensure program in Arizona, a condition of the Stipulated Agreement.

Certain Financing and Related Developments

Set forth below are descriptions of certain transactions and developments involving funding and capital that occurred in fiscal year 2022. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations - “Liquidity and Capital Resources” on page 61 for more information on our liquidity and capital resources.

a.On March 14, 2022, we raised $10 million in gross proceeds from the issuance of convertible notes. We also issued two lenders a total of $20 million in Revolving Promissory Notes which have not been drawn upon. Subsequently, the two Revolving Promissory Notes and $5 million of the proceeds from the convertible notes were pledged as collateral for the $18.3 million surety bond (see discussion above). For the fourth quarter 2022, the Company reduced marketing spend sequentially by $1.0 million, primarily to ensure sufficient collateral for the surety bond required by the Arizona State Board for Private Postsecondary Education.

b.On August 31, 2021, AGI entered into a letter agreement with The Leon and Toby Cooperman Family Foundation (“Cooperman”). On September 1, 2021, the Company borrowed $5 million from The Leon and Toby Cooperman Family Foundation (“Cooperman”) under a Credit Facility Agreement.

c.On July 21, 2021, AGI received a payment of $498,120 as a final distribution by the bankruptcy trustee in the previously disclosed Higher Education Management Group, Inc. bankruptcy proceedings. The bankruptcy filing occurred after AGI obtained a $772,793 judgment against Higher Education Management Group, Inc. No further assets are available for distribution.

Atlanta, GA Campus Approvals

On January 20, 2022, the Company announced that Aspen University received the final required state and board of registered nursing regulatory approvals for their new BSN Pre-Licensure campus location in Atlanta, Georgia. The Atlanta site was occupied by the University of Phoenix, located at 859 Mt. Vernon Highway NE, Suite 100, which is situated just off Interstate 285 in the Sandy Springs suburb in the inner ring of Atlanta. Aspen University began enrolling first-year PPN students in Atlanta starting in February 2022, and expects to enroll Nursing Core students (Years 2-3) in Fall 2022.

Accreditation

Since 1993, Aspen University has been accredited by the Distance Education Accrediting Commission ("DEAC"), an institutional accrediting agency recognized by the United States Department of Education (the "DOE") and the Council for Higher Education Accreditation ("CHEA"). On February 25, 2019, the DEAC informed Aspen University that it had renewed its accreditation for five years to January 2024.

Since 2009, USU has been accredited by WASC Senior College and University Commission ("WSCUC"), an institutional accrediting agency recognized by the DOE and the Council for Higher Education Accreditation ("CHEA"). Its current accreditation period extends through 2030.

As a result of their respective accreditations, both universities are qualified to participate under the Higher Education Act of 1965 ("HEA") and the Federal student financial assistance programs (Title IV, HEA programs).

Our operations are organized in one reporting segment.

Competitive Strengths - We believe that we have the following competitive strengths:

Proprietary Education Technology Platform – Traditionally, a University or Online Program Manager (OPM) offering online education has three core systems that serve as the backbone of their technology stack: (i) a Customer Relationship Management (CRM) system used by the enrollment team to manage prospective students; (ii) a student information system (or SIS) that the university uses to manage its student body, and (iii) a learning management system (or LMS) which serves as the online classroom.

In each of these categories, there are a number of software as a service ("SaaS") companies that offer solutions for higher education. Most universities and OPMs license one or all of these systems. In studying these systems, we concluded that there was no reasonable way to have these three separately licensed systems fluently communicate with to each other to achieve our end goal of having real-time data on every aspect of a student's career – whether it be academic in nature or personal, financial or other behavioral aspects.

As a result, several years ago we built an in-house Student Information System and connected it to our Learning Management System, D2L. We subsequently built and launched the first phase of an in-house CRM system that was designed for the enrollment departments at Aspen University and USU.

The first-phase CRM included an algorithm that recommends to Enrollment Advisors (EAs), in priority order, the follow-up calls that should be made in a given day to complete the enrollment process for prospective students in that EAs individually designated database. The algorithm was created by studying the daily habits and activities of the three most productive EAs in AGI history. This recommendation engine then automatically updates in real-time after each follow-up/action is conducted by an EA. To our knowledge, these advanced features are not offered by any CRM software company in the industry. This recommendation engine has boosted our lead conversion rates for our online nursing programs to approximately 12% vs. <10% prior to launch.

Emphasis on Online Education - The curriculum for all courses at AGI's universities is designed primarily for online delivery. Two nursing degree programs at AGI's universities require clinical practice: Aspen University's BSN Pre-Licensure hybrid (online/on-campus) nursing program and USU’s MSN-FNP hybrid (online/on-campus) nursing program. In addition, USU's Bachelor of Arts in Liberal Studies degree, Teacher Credentialing tracks require field experience/student teaching. Online, we provide students the flexibility to study and interact at times that suit their schedules. We design our online/on-campus sessions and materials to be interactive, dynamic and user friendly.

Debt Minimization - We are committed to offering among the lowest tuition rates in the sector. Our tuition rates combined with our monthly payment plan payment option for our post licensure online nursing programs has alleviated the need for a significant majority of our students to take out federal financial aid loans to fund their tuition and fees requirements.

Commitment to Academic Excellence - We are committed to continuously improving our academic programs and services, as evidenced by the level of attention and resources we apply to instruction and educational support. We are committed to achieving high course completion and graduation rates compared to competitive distance learning, for-profit schools. Regular and substantive interaction and one-on-one student contact with our highly experienced faculty brings knowledge and great perspective to the learning experience. Faculty members are available by telephone, video conference and email to answer questions, discuss assignments and provide help and encouragement to our students.

Highly Scalable and Profitable Business Model - We believe our education model, our relatively low student acquisition costs, and our flexible faculty cost model enable us to expand our operating margins. As we increase student enrollments, we are able to scale our online business on a variable basis through growing the number of full-time and adjunct faculty members after we reach certain enrollment metrics (not before). A single adjunct faculty member can work with as little as one student or as many as 50 at any given time. A full-time faculty member works with a maximum of 110 students at any given time.

We also believe our hybrid BSN Pre-Licensure Program has significant potential since there are large waiting lists of applicants at many public universities that offer BSN Pre-Licensure programs in major U.S. metropolitan areas. According to AACN’s report on 2019-2020 Enrollment and Graduations in Baccalaureate and Graduate Programs in Nursing, U.S. nursing schools turned away 80,407 qualified applicants from baccalaureate and graduate nursing programs in 2019 due to an insufficient number of faculty, clinical sites, classroom space, clinical preceptors and budget constraints.

(https://www.aacnnursing.org/Portals/42/News/Factsheets/Faculty-Shortage-Factsheet.pdf).

The Company is currently operating five pre-licensure locations in the Phoenix, Austin, Tampa, Nashville and Atlanta metros. We started operating in Phoenix in 2018. The Company opened two additional new metro locations in Fiscal Year 2021 (Austin and Tampa) and in Fiscal Year 2022 (Nashville and Atlanta), the latter of which began enrolling first year students in February 2022). We stopped admitting students into our Phoenix locations in the fourth quarter of fiscal year 2022 in accordance with the AZ BON matter.

“One Student at a Time” Personal Care - We are committed to providing our students with highly responsive and personal individualized support. Every student is assigned an Academic Advisor who becomes an advocate for the student’s success. Our one-on-one approach assures contact with faculty members when a student needs it and monitoring to keep them on course. Our administrative staff is readily available to answer any questions and work with a student from initial interest through the application process and enrollment, and most importantly while the student is pursuing their studies.

Admissions

In considering candidates for acceptance into any of our certificate or degree programs, we look for those who are serious about pursuing – or advancing in – a professional career, and who want to be both prepared and academically challenged in the process. We strive to maintain the highest standards of academic excellence, while maintaining a friendly learning environment designed for educational, personal and professional success. A desire to meet those standards is a prerequisite. Because our programs are designed for self-directed learners, successful students have a basic understanding of time management principles and practices, as well as good writing and research skills. Admission to Aspen University is based on a thorough assessment of each applicant’s potential to complete the program successfully.

Industry Overview

According to the DOE reports, among college students that study exclusively online, the percentage of students at private for-profit institutions was higher (60%), than that of students at public institutions (46%) and private nonprofit institutions (34%). In particular, the percentage of students who took distance education courses exclusively was highest at private for-profit four-year institutions (73%) which, despite enrolling only 4% of undergraduates, accounted for 6% of undergraduates who were enrolled exclusively in distance education courses.

In terms of the nursing sector, job opportunities for registered nurses are expected to grow about as fast as the average growth for all occupations, or approximately 9%, between 2020 and 2030, according to the U.S. Bureau of Labor Statistics’ Occupational Outlook Handbook, 2020-30 Edition. However, despite the anticipated growth in job opportunities, over 80,400 qualified applications were not accepted by entry-level baccalaureate and graduate nursing programs according to the 2019-2020 Enrollment and Graduations in Baccalaureate and Graduate Programs in Nursing report from the American Association of Colleges of Nursing (https://www.aacnnursing.org/Portals/42/News/Factsheets/Faculty-Shortage-Factsheet.pdf). These statistics suggest there continues to be unmet demand from qualified students for nursing educational programs. In fiscal year 2022, nursing shortages continued in part due to ongoing effects of the COVID-19 pandemic. A growing number of nurses are leaving the profession as they reach retirement age or due to pandemic-induced job fatigue. This supply-side trend, coupled with the rising demand for healthcare to support the aging U.S. population, is expected to perpetuate a nursing shortage through 2030. Given the growing demand for healthcare services across a multitude of specialties, reports project that 1.2 million new registered nurses (RNs) will be needed by 2030 to address the current shortage.

Competition

According to the most recent 2019 Digest of Education Statistics (nces.ed.gov), there are more than 4,300 U.S. colleges and universities serving traditional college-age students and adult students. Any reference to universities herein also includes colleges. Competition is highly fragmented and varies by geography, program offerings, delivery method, ownership, quality level, and selectivity of admissions. No one institution has a significant share of the total postsecondary market. While we compete in a sense with traditional “brick and mortar” universities, our primary competitors are universities that primarily enroll online students. Our primarily online university competitors include American Public Education, Inc. (Nasdaq: APEI), Adtalem Global Education (NYSE: ATGE), Apollo Education Group, Inc., Grand Canyon Education, Inc. (Nasdaq: LOPE), Strategic Education, Inc. (Nasdaq: STRA), and Western Governors University.

We believe that these competitors have degreed enrollments ranging from approximately 38,000 to over 100,000 students. As of April 30, 2022, AGI had 13,334 active degree-seeking students enrolled. Because of COVID-19 which has caused most

educational institutions to transition to some extent to more online capabilities, we may face more online competition in the future. Further, COVID-19 caused nurses to seek graduate level courses to retrench as they were overwhelmed treating hospitalized patients. COVID-19 also significantly reduced the number of students enrolled in postsecondary education institutions in recent years, which limits the pool of prospective students for which we compete for enrollments with our competitors in the industry.

The primary mission of most traditional accredited four-year universities is to serve full-time students and conduct research. Most online universities serve working adults. Aspen Group acknowledges the differences in the educational needs between working and full-time students at “brick and mortar” schools and provides programs and services that allow our students to earn their degrees without major disruption to their personal and professional lives.

We also compete with public and private degree-granting regionally and nationally accredited universities. An increasing number of universities enroll working students in addition to the traditional 18 to 24-year-old students, and we expect that these universities will continue to modify their existing programs to serve working learners more effectively, including by offering more distance learning programs. We believe that the primary factors on which we compete are the following:

•Active and relevant curriculum that considers the needs of employers;

•The ability to provide flexible and convenient access to programs and classes;

•Cost of the program;

•Monthly payment plan options;

•High-quality courses and services;

•Comprehensive student support services;

•Breadth of programs offered;

•The time necessary to earn a degree;

•Qualified and experienced faculty;

•Reputation of the institution and its programs;

•The variety of geographic locations of campuses;

•Name recognition; and

•Convenience.

Academics

Aspen University

School of Nursing and Health Sciences

School of Education

School of Business and Technology

School of Arts and Sciences

United States University

College of Nursing and Health Sciences

College of Business and Technology

College of Education

Sales and Marketing

Following Mr. Michael Mathews becoming our Chief Executive Officer in 2011, he and his team made significant changes to Aspen’s sales and marketing program, specifically spending a significant amount of time, money and resources on our proprietary Internet marketing program. What is unique about our Internet marketing program is that we have not used and have no plans in the near future to acquire non-branded, non-exclusive leads from third-party online lead generation companies to attract prospective students. To our knowledge, most if not all for-profit online universities utilize multiple third-party online lead generation companies to obtain a meaningful percentage of their prospective student leads that are branded and exclusive in nature, and those leads are both non-branded and non-exclusive in addition to exclusive branded leads. Our executive officers have many years of expertise in the online lead generation and Internet advertising industry, which has and for the foreseeable future is expected to continue to allow us to cost-effectively drive all prospective student leads that are branded and exclusive in nature.

We have invested in our technology infrastructure and believe our education technology platform enables us to achieve lower costs per enrollment as compared to our competition.

Human Capital

We recognize that our performance depends on the education, experiences, and efforts of our employees, and our ability to foster a culture that brings out the best in each. As of April 30, 2022, we had 312 full-time employees, including full-time faculty, and 821 adjunct professors, who are part-time employees. None of our employees are parties to any collective bargaining arrangement. We believe our relationships with our employees are good. Our employees have diverse backgrounds, as evidenced by the fact that approximately 74% of our faculty and staff are female and approximately 48% of our employees self-identify as ethnically diverse.

Diversity and equity are at the heart of our culture, influenced in part by the communities we serve including but not limited to healthcare, the military, and veterans. In support of their respective missions, each of our universities have published diversity and equity statements that guide and support their actions to attract, retain and develop highly qualified administration, faculty, and staff:

Aspen University is committed to diversity, equity, and inclusion in its faculty, administration, and staff hiring practices, employee policies, and student admissions practices and policies. It is committed to non-discrimination in the delivery of its educational services and employment opportunities. The University does not discriminate on the basis of sex, race, color, national origin, religion, age, gender, sexual orientation, veteran status, physical or mental disability, medical condition as defined by law, or any basis prohibited by law.

As forged by its mission and vision and the University’s unique and distinctive character to serve the underserved community in California and the nation, United States University ensures an uncompromising commitment to offering access to affordable higher education to all individuals who meet the criteria for admission regardless of age, gender, culture, ethnicity, socio-economic class and disability. At all times, USU shall strive to ensure equitable representation of all diverse groups in its student body. USU’s diverse administration, faculty and staff shall be equally dedicated to the success of all students. The diversity of USU’s administration and faculty shall help enrich curricula, while a diverse staff shall serve students with sensitivity to special needs.

We have learned that an inclusive and positive workplace results in business growth and inspires increased academic and business innovation, the retention of exceptional talent, and a more involved workforce.

Talent Development and Retention

The Company is dedicated to attracting, retaining, and developing employees who adhere to high standards of business and personal integrity and who maintain a reputation for honesty, fairness, respect, responsibility, and trust. Our strategic initiatives require our leadership, management, faculty, and staff to perform at a consistently high level and to adapt and learn new skills and capabilities. Our employees must have a wide and diverse range of education, experience, background, and skill to anticipate and meet our business needs and exercise sound business judgment.

To promote retention, we offer comprehensive compensation and benefits packages that are competitive and performance-based. We have undertaken an analysis of market-competitive compensation and benefits practices to attract new and more culturally diverse employees and to reward current ones. We believe that continuous education aids in employee retention and so we provide a tuition benefit to them, their spouses, or their dependents. Full-time employees receive a 100% tuition discount on most programs offered by the universities. Spouses, legal partners, and legal dependents of full-time employees, as well as adjunct faculty, receive a 50% discount.

To promote career development among our leadership and staff, we provide job and leadership training as well as professional development opportunities. We financially support university administration and management as they seek professional development through professional organizations relevant to their fields and conference attendance. We financially support faculty professional development to stay current in their field of study through NurseTim© trainings (nursing faculty only) and conference attendance. The Faculty Speaker Series, Tuesday Teaching Tips, and Research Colloquium, all supported through the Center for Graduate Studies, also contribute to the professional development of faculty.

We believe that our well-educated and well-qualified faculty are the basis for the success of our students and our programs. Because our business is primarily nursing education, we expect our faculty to integrate their personal and professional nursing experiences into the education of our students. All nursing faculty maintain current, unencumbered state or multi-state compact RN licenses. All faculty are expected to have a degree one level above the degree level they are teaching and to maintain currency in their field. We train and develop our faculty through a formal onboarding process that includes orienting them to academic policies and procedures, pedagogical performance expectations, and responsibilities related to their faculty role. They

also receive training in tools for increasing student engagement and specific technologies they are required to use for various purposes. After their training, the universities regularly review the performance of their faculty by, among other things, monitoring the contact that faculty have with students, reviewing student feedback, and evaluating the learning outcomes achieved by students. As a result of our training and professional development practices for faculty, we have very little turnover and faculty retention is high.

Over time, we have hired, retained, and developed a diverse leadership, management, and workforce that is a key component of our success and culture. We believe that our success is directly correlated to our ability to provide employees an interesting and engaging work experience. We value our rich, diverse employees and provide career and professional development opportunities that foster the success of our company.

Impact of COVID-19

The health and well-being of our employees is of utmost importance to the Company. Starting in March 2020, all employees transitioned to a remote workforce. Since that time, Company employees have demonstrated resilience, wisdom, commitment, and compassion in working with colleagues and students. Beginning on June 1, 2021, in an abundance of caution, employees in the U.S. were allowed to return to their offices after providing proof of full vaccination. As of July 6, 2021, all U.S. employees began returning to their offices in a hybrid work environment, meaning that employees now work 40% from home and 60% from the office. Each team within the Company has been given the flexibility to work with their management to determine which days and/or weeks will be worked from home vs. office. Employees are required to follow all Centers for Disease Control and Prevention and local guidelines and federal regulations. Finally, the Company has also introduced a fully-remote model for certain high-performance employees, what the Company calls the ‘Meritocracy Benefit’.

Corporate History

The Company was incorporated on February 23, 2010 in Florida. In February 2012, Aspen Group reincorporated in Delaware under the name Aspen Group, Inc.

Aspen University Inc. was incorporated on September 30, 2004 in Delaware. Its predecessor was a Delaware limited liability company organized in Delaware. On March 13, 2012, Aspen Group, which was then inactive, acquired Aspen University Inc. in a transaction we refer to as the reverse merger. On December 1, 2017, Aspen Group acquired USU.

Available Information

Our corporate website is www.aspu.com. On our website under "SEC Filings", we make available access to our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Proxy Statements on Schedule 14A and amendments to those materials filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), free of charge.

Regulation

Regulatory Environment

Students attending our schools finance their education through a combination of individual resources, corporate reimbursement programs and federal student financial assistance funds available through our participation in the Title IV Programs. The discussion which follows outlines the extensive regulations that affect our business. Complying with these regulations entails significant effort from our executives and other employees. Further, regulatory compliance is also expensive. Beyond the internal costs, compliance with the extensive regulatory requirements also involves engagement of outside regulatory professionals.

To participate in Title IV Programs, a school must, among other things, be:

•Authorized to offer its programs of instruction by the applicable state education agencies in the states in which it is physically located (in our case, Colorado, Arizona, Texas, Florida, Georgia, Tennessee and California) or otherwise have a physical presence as defined by the state and meet the state education agency requirements to legally offer postsecondary distance education in any state in which the school is not physically located;

•Accredited by an accrediting agency recognized by the Secretary of DOE; and

•Certified as an eligible institution by DOE.

Collectively, state education agencies, accrediting agencies, and the DOE comprise the higher education regulatory triad. We cannot predict the actions that any entity in the higher education regulatory triad, Congress, or Administration may take or their effect on our schools.

State Authorization

As institutions of higher education that grant degrees and certificates, we are required to be authorized by applicable state education authorities which exercise regulatory oversight of our schools. In addition, in order to participate in the Title IV Programs, we must be authorized by the applicable state education agencies.

Because we are subject to extensive regulations by the states in which we become authorized or licensed to operate, we must abide by state laws that typically establish standards for instruction, qualifications of faculty, administrative procedures, marketing, recruiting, financial operations and other operational matters. State laws and regulations may limit our ability to offer educational programs and to award degrees. Some states may also prescribe financial regulations that are different from those of DOE. If we fail to comply with state licensing requirements, we may lose our state licensure or authorizations, which in turn would result in a loss of accreditation and access to Title IV funds.

The California Legislature is currently considering the reauthorization of the California Bureau for Private Postsecondary Education (“California Bureau”) as part of its sunset review cycle. There is currently a bill in process (SB1433) that would amend the existing Private Postsecondary Education Act, which governs private institutions operating in the state. On June 22, 2022, SB1433 was amended to include a number of updated definitions, substantive changes around minimum operating standards, and amended accreditation requirements for degree granting institutions, among other amendments. The Bill is set for a hearing in the Assembly Business and Professions committee on June 28th. We expect there will be additional amendments following the hearing, and we do not know what the final version of the bill will include or whether it will be approved by the Governor. In prior years, there have been multiple onerous bills proposed in California that have not become law, and we cannot predict whether similar proposals may be integrated into the current proposal as it moves through the legislative process. Other states in which AGI operates may also make material changes to their authority and structure at any time, so AGI must constantly assess its state oversight agencies to ensure compliance.

Licensure of Online Programs

On July 31, 2018, the DOE announced its intention to convene a negotiated rulemaking committee (the “Committee”) to consider proposed regulations for Title IV Programs, including revisions to the 2016 state authorization of distance education regulations. The Committee convened for several meetings from January to April 2019. On June 12, 2019, the DOE published a notice of proposed rulemaking, which included proposed regulations that would supplant the 2016 regulations. The DOE released final regulations on accreditation and state authorization of distance education on November 1, 2019, which took effect July 1, 2020 (the “Final Regulations”). Like the 2016 regulations, the Final Regulations require Title IV Program institutions, like ours, that offer postsecondary education through distance education to students in a state in which the institution is not physically located or in which it is otherwise subject to state jurisdiction as determined by that state, to meet any state requirements to offer postsecondary education to students who are located in that state.

Under the Final Regulations, institutions may meet the authorization requirements by obtaining such authorization directly from any state that requires it or through a state authorization reciprocity agreement, such as the State Authorization Reciprocity Agreement (“SARA”). SARA is intended to make it easier for students to take online courses offered by postsecondary institutions based in another state. SARA is overseen by a National Council (“NC-SARA”) and administered by four regional education compacts.

In May 2022, resulting from its formal move from Colorado to Arizona, Aspen University was removed as an approved institutional participant in NC-SARA through CO-SARA. An agreement with CO-SARA permits most currently enrolled students to be covered through early September 2022. Aspen University will be on the agenda for AZ-SARA in early September 2022 to obtain approval to become an institutional participant again in NC-SARA from its new primary location in Arizona. In the meantime, Aspen University is seeking individual state authorizations for its students. Aspen University is currently authorized in 30 states and is in the development process with 20 states and the District of Columbia. Aspen maintains its state authorizations through annual reporting and required renewals. The only state that does not participate in NC-SARA is California and it has imposed regulatory requirements on out-of-state educational institutions operating within its boundaries, such as those having a physical facility or conducting certain academic activities within the state. Aspen University is registered as an out-of-state institution with California until February 19, 2023, and plans to renew at that time. Aspen University currently enrolls students in all 50 states. While we do not believe that any of the states in which our schools are currently licensed or authorized, other than Arizona, Texas, Florida, Georgia, Tennessee and California, is individually material to our

operations, the loss of licensure or authorization in any state could prohibit us from recruiting prospective students or offering services to current students in that state, which could significantly reduce our enrollments.

On July 14, 2020, the Delaware DOE informed Aspen that an application for renewal was not necessary due to its active institutional membership with NC-SARA. With Aspen’s removal as an active institutional member of NC-SARA in May 2022, Aspen currently seeks renewal in the State of Delaware.

Because USU is based in California, which does not participate in NC-SARA, USU must obtain authorization in every state in which it intends to market and enroll online students, which was the standard method prior to the formation of NC-SARA. USU is currently authorized to offer one or more programs in 42 states and is in the application development process with 8 additional states and the District of Columbia. USU maintains its state authorizations through annual reporting and required renewals.

Individual state laws establish standards in areas such as instruction, qualifications of faculty, administrative procedures, marketing, recruiting, financial operations, and other operational matters, some of which are different than the standards prescribed by the Arizona Board, the Texas Board, the Florida Commission, the Tennessee Commission, the Georgia Commission, and the California Bureau. Laws in some states limit the ability of schools to offer educational programs and award degrees to residents of those states. Some states also prescribe financial regulations that are different from those of DOE, and many require the posting of surety bonds. Laws, regulations, or interpretations related to online education could increase our cost of doing business and affect our ability to recruit students in particular states, which could, in turn, negatively affect enrollments and revenues and have a material adverse effect on our business.

Licensure of Physical Locations

The Higher Education Opportunity Act ("HEOA") and certain state laws require our institutions to be legally authorized to provide educational programs in states in which our schools have a physical location or otherwise have a physical presence as defined by the state. Aspen University is authorized to provide educational programs in Arizona by the Arizona State Board for Private Postsecondary Education (“Arizona Board”), in Texas by the Texas Higher Education Coordinating Board (“Texas Board”), in Tennessee by the Tennessee Higher Education Commission (“Tennessee Commission”), in Georgia by the Georgia Nonpublic Postsecondary Education Commission (“Georgia Commission”), and in Florida by the Florida Commission on Independent Education (“Florida Commission”). USU is authorized to provide educational programs in California by the California Bureau. Failure to comply with state requirements could result in Aspen University losing its authorization from the Arizona Board, Texas Board, Tennessee Commission, Georgia Commission, or Florida Commission; and USU losing its authorization from the California Bureau. In such event, the schools would lose their eligibility to participate in Title IV Programs, or their ability to offer certain educational programs, any of which may force us to cease the school’s operations.

Additionally, Aspen University and USU are Delaware corporations. Delaware law requires an institution to obtain approval from the Delaware Department of Education, or Delaware DOE, before it may incorporate with the power to confer degrees. In July 2012, Aspen University received notice from the Delaware DOE that it was granted provisional approval status effective until June 30, 2015. On April 25, 2016, the Delaware DOE informed Aspen University it was granted full approval to operate with degree-granting authority in the State of Delaware. On July 14, 2020, the Delaware DOE informed Aspen that an application for renewal was not necessary due to its active institutional membership with NC-SARA. With Aspen’s removal as an active institutional member of NC-SARA in May 2022, Aspen currently seeks renewal in the State of Delaware. On June 6, 2018, the Delaware DOE granted an initial operating license to USU until June 30, 2023.

In March 2022, Aspen entered into a Consent Agreement with the AZ BON resulting primarily from concerns raised by the AZ BON stemming from NCLEX-RN pass rates below the state’s required threshold. The result of the Consent Agreement is that Aspen University remains approved with the AZ BON based on a stayed revocation and probationary period with certain conditions, including but not limited to, the cessation of enrollments in the core component of the pre-licensure nursing program and reporting to staff/board on a monthly basis. The cessation of enrollments into the core component of the pre-licensure nursing program will remain in effect until Aspen University complies with the conditions of its Consent Agreement with the AZ BON, which is more fully discussed under “State Professional Licensure” below. In April 2022, Aspen University entered into a Stipulated Agreement with the Arizona State Board for Private Postsecondary Education as an amendment to its 2022 Regular Vocational and Degree Granting Agreement for licensure. The Stipulated Agreement required the cessation of enrollments in both the pre-professional nursing and core components of the pre-licensure program in Arizona, the posting of a surety bond in the amount of $18,287,110 which has already been posted, the submission of student records on a monthly basis, and the removal of the Arizona pre-licensure nursing program start date information from its website and marketing materials. Aspen University is not currently enrolling students in the BSN Pre-licensure program in Arizona. The Stipulated Agreement can be amended in the future.

Accreditation

Aspen University is institutionally accredited by the DEAC, an accrediting agency recognized by CHEA and the DOE, and USU is institutionally accredited by WSCUC, an accrediting agency also recognized by CHEA and the DOE. Accreditation is a non-governmental system for evaluating educational institutions and their programs in areas including student performance, governance, integrity, educational quality, faculty, physical resources, administrative capability and resources, and financial stability. In the U.S., this recognition comes primarily through private voluntary associations that accredit institutions and programs. To be recognized by the DOE, accrediting agencies must adopt specific standards for their review of educational institutions. Accrediting agencies establish criteria for accreditation, conduct peer-review evaluations of institutions and programs for accreditation, and publicly designate those institutions or programs that meet their criteria. Accredited institutions are subject to periodic review by accrediting agencies to determine whether such institutions maintain the performance, integrity and quality required for accreditation.

Accreditation is important to our schools for several reasons. Accreditation provides external recognition and status. Employers rely on the accredited status of institutions when evaluating an employment candidate’s credentials. Corporate and government sponsors under tuition reimbursement programs look to accreditation for assurance that an institution maintains quality educational standards. Other institutions depend, in part, on our accreditation in evaluating transfers of credit and applications to graduate schools.

Moreover, institutional accreditation awarded from an accrediting agency recognized by DOE is necessary for eligibility to participate in the Title IV Programs. As part of the Final Regulations published on November 1, 2019, and which took effect July 1, 2020, the DOE amended regulations relating to the recognition of accrediting agencies. The Final Regulations amended the DOE’s process for recognition and review of accrediting agencies, including the criteria used by the DOE to recognize accrediting agencies, and the DOE’s requirements for accrediting agencies’ policies and standards that are applied to institutions and programs. Accrediting agencies are under heightened scrutiny due to perceived shortcomings of certain agencies and their oversight of closed institutions. In response, accreditors are increasing their scrutiny of institutions. From time to time, accrediting agencies adopt or make changes to their policies, procedures and standards. If our schools fail to comply with any of these requirements, the non-complying school’s accreditation status could be at risk.

In addition to institutional accreditation, there are numerous specialized accreditors that accredit specific programs or schools within their jurisdiction, many of which are in healthcare and professional fields. USU’s and Aspen University’s baccalaureate and master’s degree programs in nursing are accredited by the Commission on Collegiate Nursing Education (CCNE) and Aspen University’s doctoral nursing degree is currently CCNE-accredited. CCNE is officially recognized by CHEA and the DOE and provides accreditation for nursing programs. Accreditation by CCNE signifies that those programs have met the additional standards of that agency. We are also pleased that Aspen University’s School of Business and Technology has been awarded the status of Candidate for Accreditation by the International Accreditation Council for Business Education (IACBE) for its baccalaureate and master’s business programs. Finally, USU’s Bachelor of Arts in Liberal Studies has two Teacher Credentialing tracks: (1) Multiple Subject Credential Preparation track for students in California interested in teaching at the TK-6 level, and (2) General track for students interested in exploring a variety of topics, transfer students, or students outside of California. Both tracks are approved by the California Commission on Teacher Credentialing (CTC).

If we fail to satisfy the standards of specialized accreditors, we could lose the specialized accreditation for the affected programs, which could result in materially reduced student enrollments in those programs and prevent our students from seeking and obtaining appropriate licensure in their fields.

State Professional Licensure

States have specific requirements that an individual must satisfy in order to be licensed or certified as a professional in specific fields. For example, graduates from some USU and Aspen University nursing programs often seek professional licensure in their field because they are legally required to do so in order to work in that field or because obtaining licensure enhances employment opportunities. Success in obtaining licensure depends on several factors, including each individual’s personal and professional qualifications as well as other factors related to the degree or program completed, including but not necessarily limited to:

•whether the institution and the program were approved by the state in which the graduate seeks licensure, or by a professional association;

•whether the program from which the applicant graduated meets all state requirements; and

•whether the institution and/or the program is accredited by a CHEA and DOE-recognized agency.

Professional licensure and certification requirements can vary by state and may change over time.

In addition, the Final Regulations that took effect July 1, 2020 require institutions to make readily available disclosures to enrolled and prospective students regarding whether programs leading to professional licensure or certification meet state educational requirements for that professional license or certification. These disclosures apply to both on-ground and online programs that lead to professional licensure or certification or are advertised as leading to professional licensure or certification. Under the Final Regulations, institutions must determine the state in which current and prospective students are located, and then must: (1) determine whether such program’s curriculum meets the educational requirements for licensure or certification in that state; (2) determine whether such program’s curriculum does not meet the educational requirements for licensure or certification in that state; or (3) choose not to make a determination as to whether such program’s curriculum meets the educational requirements for licensure or certification in that state. Institutions must also provide direct disclosures in writing to prospective students and current students under certain circumstances. Institutions must provide direct disclosures in writing to prospective students if the institution has determined the program in which the student intends to enroll does not meet the educational requirements for licensure or certification in the state in which the student is located or if the institution has not made any determination. Institutions must provide direct disclosures in writing to current students, but only if the institution has determined the program in which the student is enrolled does not meet the educational requirements for licensure in the state in which the student is located.

As noted above, in March 2022, Aspen University entered into the Consent Agreement with the AZ BON. Aspen University held provisional approval to offer the core component of its pre-licensure nursing program in Arizona through AZ BON; in June 2022, the AZ BON granted approval of Aspen University’s request for provisional approval as long as the program is in compliance with the consent agreement through March 31, 2025. However, Aspen University is not currently enrolling students in the BSN Pre-licensure program in Arizona. While Aspen University disputed many of the allegations made, the institution determined that settlement was the best option to reduce disruption for students and address the concerns raised. As a condition of the Consent Agreement, Aspen University’s Provisional Approval was revoked, with the revocation stayed pending Aspen University’s compliance with the terms and conditions of the Consent Agreement. The stay is broken into two phases, the first lasting through the end of Calendar Year 2022. During Phase I, Aspen University is not permitted to enroll any new students into the core component of its pre-licensure nursing program in Arizona, and must achieve the AZ BON-required 80% NCLEX pass rate for the Calendar Year 2022 annual reporting cycle. If this benchmark is not achieved, the AZ BON may lift the stay and initiate the revocation. If Phase I is completed successfully, Phase II will commence with Aspen University on Probation (regular or “stayed revocation” probation, depending on the outcome of Phase I). Aspen University is permitted to begin enrollments into the core component of its pre-licensure nursing program in Arizona once four consecutive quarters of 80% NCLEX first-time pass rates occur. However, once achieved, if the NCLEX pass rate falls below 80% for any quarter, the AZ BON may limit enrollments, and repeated failures may result in a required cessation of enrollments and teach-out of the program. The terms of the Consent Agreement also include requirements that we provide the AZ BON with monthly reports, provide that our faculty and administrators undergo additional training, retain an approved consultant to prepare and submit evaluations to the AZ BON, and hire a minimum of 35% full-time qualified faculty by September 30, 2022. The Consent Agreement is filed as Exhibit 10.22 to this Report. For the quarters ended March 31, 2022 and June 30, 2022, Aspen University’s NCLEX scores were 73.33% and 69.64%, respectively.

Nature of Federal, State and Private Financial Support for Postsecondary Education

The federal government provides a substantial part of its support for postsecondary education through the Title IV Programs, in the form of grants and loans to students. Students can use those funds at any institution that has been certified by DOE to participate in the Title IV Programs. Aid under Title IV Programs is primarily awarded on the basis of financial need, generally defined as the difference between the cost of attending the institution and the amount a student can reasonably contribute to that cost. All recipients of Title IV Program funds must maintain satisfactory academic progress and must progress in a timely manner toward completion of their program of study. In addition, each school must ensure that Title IV Program funds are properly accounted for and disbursed in the correct amounts to eligible students.

Our institutional missions manifest themselves through offering students the opportunity to fund their education without relying solely on student loans. In 2014, Aspen University launched a $250 monthly payment plan for associate and bachelor degree students and a $325 monthly payment plan for master’s degree students, and subsequently a $375 monthly payment plan for doctoral and MSN-FNP students. The monthly payment plan is available to all Aspen University and United States University students except those in the Aspen University BSN Pre-Licensure program.

Currently, 6,811 or 67% of Aspen University students utilize monthly payment options, including the monthly payment plan or the installment plan. In 2017, USU implemented these monthly payment options and currently has 2,148 or 69% of its students utilizing them.